SMT Line Case Study: Fixing Manufacturing Product Costing

When electronics printed circuit board (PCB) assembly manufacturer asked me to review its costing and operations, management believed they already knew the root cause of their financial and operational problems.

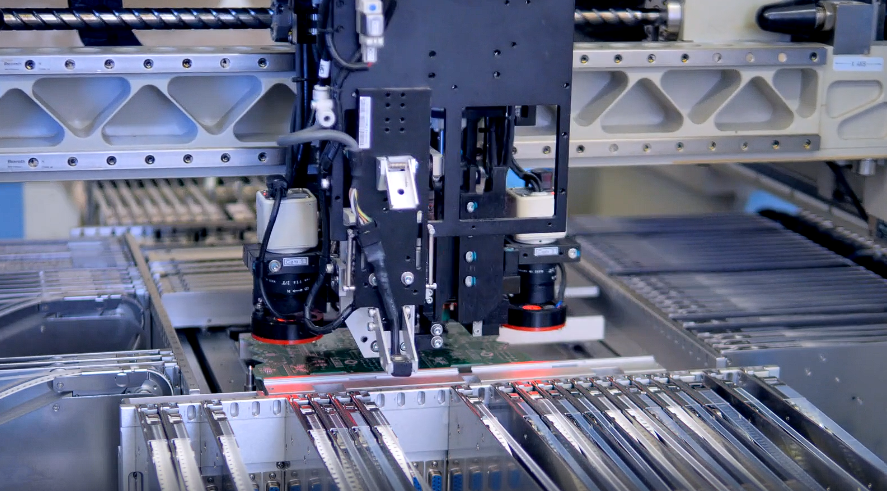

The Surface Mount Technology (SMT) line was ageing. The pick-and-place machine suffered frequent breakdowns in fact it was a second hand 10 years old. Production was consistently behind schedule, and customer lead times were increasing. The proposed solution seemed straightforward: replace the entire SMT line.

However, the capital investment required was substantial, and the business lacked the cash flow to fund it internally. The expectation was that the parent company would step in to finance the project.

Before recommending a major capital expenditure project, I carried out a detailed review of the company’s costing model, production processes, and shop-floor operational performance. The findings revealed that the ageing SMT line was not the biggest issue facing the business.

Was the SMT Line Really the Manufacturing Bottleneck?

No. While the SMT line experienced genuine reliability issues, it was not the primary constraint limiting total throughput or profitability.

Like many manufacturers, management had focused heavily on the most visible problem. Frequent machine stoppages naturally attracted attention because they disrupted production schedules and created immediate frustration across the organisation.

However, bottlenecks are rarely found where the noise is loudest.

After reviewing the end-to-end production flow across the facility, it became clear that the real operational constraint existed downstream.

The through-hole assembly process relied heavily on manual labour, with approximately 15 to 20 operators assembling customised products. Work-in-progress (WIP) was accumulating heavily in this area, creating massive queues, delays, and extended lead times throughout the entire operation. While management focused on machine downtime within SMT, the true capacity constraint sat in manual assembly.

Were the ERP Standard Product Costs Accurate?

No. The standard costing system contained significant inaccuracies that completely distorted profitability reporting and strategic decision-making.

The company operated an integrated Enterprise Resource Planning (ERP) system with standard costing functionality. Management naturally assumed the reported product costs were reliable because they originated from an advanced software system.

Unfortunately, the underlying data and accounting assumptions had not been reviewed since the ERP system went live years prior.

A deep product cost analysis identified four critical errors:

- Averaged Machine Rates: Machine hour rates had been blended across the entire SMT line, masking the true resource consumption of individual boards.

- Outdated Fixed Costs: Factory overhead allocation was based on historical assumptions made during the initial implementation, failing to account for inflation in energy, rent, and wages and all other related costs.

- Unit-of-Measure (UOM) Errors: Bills of Materials (BOM) contained severe entry errors; some electronic components were costed as individual units, while others were costed as entire component reels.

- Stale Manufacturing Standards: Standard costs had never been updated to reflect subtle, ongoing operational shifts.

The result was a costing model failed to reflect the true economics of manufacturing each unit, meaning key commercial decisions were being made using completely unreliable information.

How Was Production Scheduling Affecting Profitability?

The company’s make-to-order scheduling approach created excessive setup times, reduced overall factory capacity, and increased operational inefficiency.

While a make-to-order model is entirely standard in electronics manufacturing, jobs were being scheduled individually on an order-by-order basis. They were not grouped into logical product families. This fragmented approach dramatically increased:

- Machine setup frequency and downtime

- Production floor interruptions

- Manual material handling

- Scheduling and planning complexity

- Lost productive capacity

By grouping similar products together into product families, setup frequency could be slashed and available manufacturing capacity increased immediately without requiring a single penny of capital expenditure.

What Impact Did the Costing Review Have on Profit Margin?

The implementation of data-driven costing and process improvements delivered a 13% improvement in gross profit margin without purchasing a new SMT line.

Before the review, management expected net profit margins of approximately 15%. The real financial data told a very different story: achieving even a 5% net profit was a struggle, and several months were entirely loss-making.

The Operational and Financial Impact Analysis

| Operational Issue | Real-World Impact on the Business |

| Extended Lead Times | 5–7 week delivery delays and strained customer relationships. |

| Poor Costing Accuracy | Misleading profitability information on core revenue-generating products. |

| Uncontrolled Labour Growth | Additional operators continually added to through-hole areas to manage delays. |

| Severe Cash Flow Pressure | Reduced financial flexibility and trapped working capital. |

| Production Bottlenecks | Hidden constraints leading to lost throughput and delivery issues. |

After completely redesigning the product costing model, correcting the Unit of measure errors in the BOM, reassessing machine cost allocations, creating product families, and restructuring the manual through-hole assembly process, management finally gained a clear view of true operational performance. Commercial decisions shifted to concrete data.

What Can Manufacturers Learn From This Case?

The most visible operational problem is rarely the root cause of margin erosion. Accurate product costing and meticulous bottleneck analysis routinely reveal opportunities that are completely hidden beneath daily floor issues.

When performance deteriorates, many manufacturing directors immediately turn to expensive capital expenditure projects. While equipment upgrades are sometimes necessary, businesses must first challenge their data by asking five critical questions:

- Are our current product costs completely accurate?

- Have our ERP costing standards been audited recently?

- Do we truly understand our primary manufacturing bottleneck?

- Are our production scheduling methods supporting floor efficiency?

- Are we making high-level commercial decisions using reliable data?

In this case, the business was prepared to pursue an expensive SMT replacement project. Our analysis proved that the expected benefits would have been non-existent because the real constraint sat further down the line.

A thorough understanding of costing, capacity, and operational flow unlocked substantial cash and profitability using existing machinery.

Conclusion

Manufacturing performance problems are rarely solved by simply replacing a single machine. More frequently, they stem from outdated data, inaccurate costing structures, inefficient scheduling practices, and misunderstood bottlenecks.

For this PCB assembly manufacturer, the turnaround did not require a new SMT line. It required gaining absolute visibility into what was actually happening inside the business. The result was improved profitability, robust operational decision-making, and a much clearer path for future capital investment.

Before committing to expensive equipment upgrades, manufacturers must ensure they fully understand their true costs, structural constraints, and operational drivers.

Reclaim Your Manufacturing Margins

If your expected margins are not translating into cash in the bank, it is time to audit your product costing structure and uncover your true operational bottlenecks.

- Book a Discovery Call: https://calendly.com/skynet-skynetaccounting/new-meeting

- Connect on LinkedIn: www.linkedin.com/in/skynet-yesim-tilley

- Visit Our Website: www.skynetaccounting.co.uk

About the Author

Yesim Tilley ACMA, CGMA is the Founder of Skynet Accounting and a Chartered Management Accountant with over 20 years’ experience supporting UK manufacturing, engineering and industrial businesses. Driving manufacturing profit through better product costing, ERP costing validation and financial strategy, she helps manufacturers improve margins, cash flow and long-term profitability. She is also the author of How to Unlock Cash to Fuel Manufacturing Success.